Mobile Money

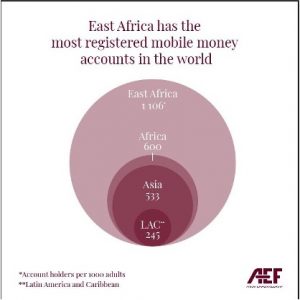

East africa

East Africa, in particular Kenya, Rwanda, Tanzania, and Uganda, has the world’s highest mobile money penetration rate. For every 1,000 adults in the region, there are 1,106 registered mobile money accounts, compared to 600 for the whole of Africa, 533 for Asia, and 245 for Latin America and the Caribbean.

The number of mobile money agents in Kenya has increased from 307 in March 2007, to over 240,000 in March 2020.

In 2015, the volume of transactions using M‑PESA, a mobile domestic money transfer and financing service from the region, reached 45% of Kenya’s GDP. Companies such as M-KOPA provide affordable electricity from solar power, which has reached 750,000 homes and businesses across East Africa.

Central Africa

Gabon, as a precursor, has successfully invested in the development of undersee cables, landing stations, and a terrestrial network. As a result, since 2010, the number of internet users has increased sevenfold. In addition, the cost of internet access has been reduced by a factor of 10, resulting in an increase in Internet Penetration from 28% to 48%.

“The unrealized potential of Central Africa can be fulfilled through regional investments in digital infrastructure that enhance internet availability and affordability. It would ease the school-to-digital-work transition through public-private collaborations as well.”

North Africa

West Africa

South Africa

Conclusion

Africa’s digital transformation points to a favourable trend. However, as many regions and countries seem to improve their infrastructure, a huge lack in transferring the resulting technologies to the population still exists. The fact that only a small percentage of companies have a website demonstrates, on one hand, how difficult it is to afford the necessary devices. And, on the other hand, the lack of expertise to create them.

With the right policies and measures, Africa’s full potential may be realized, allowing it to address many of its problems. Africa’s technological infrastructure should be used to bring more women into the labour market and shrink the gender gap. It should provide education to people in rural areas, encourage the youth to learn computer skills, and create more jobs and opportunities.

By Djamal Gandi

Resources

- AUC/OECD (2021), Africa’s Development Dynamics 2021: Digital Transformation for Quality Jobs, AUC, Addis Ababa/OECD Publishing, Paris, https://doi.org/10.1787/0a5c9314-en, https://doi.org/10.1787/cd08eac8-fr

- GSMA, State of the Industry Report on Mobile Money 2021

https://www.gsma.com/sotir/ - Fritzsche, Kerstin & Shuttleworth, Luke & Brand, Bernhard & Blechinger, Philipp. (2019). Exploring the nexus of mini-grids and digital technologies.

https://www.researchgate.net/publication/338646545 - ITU-Publications, Digital Trends in Africa 2021: Information and communication technology trends and developments in the African region 2017 – 2020

https://toolkit-digitalisierung.de/app/uploads/2021/04/Digital-trends-in-Africa-2021.pdf